The numbers are staggering, and they tell a story of economic devastation that will take years to fully comprehend. According to a United Nations Development Programme (UNDP) report published on March 31, 2026, the first month of the US-Israel war on Iran cost Arab economies an estimated $120 billion to $194 billion in lost gross domestic product. This represents a contraction of approximately 3.7 to 6 percent of the region's GDP.

The human cost is equally severe. The UNDP estimated that 3.7 million jobs were lost across the region, with approximately four million more people pushed below the poverty line. The report highlighted the "fragility in the Arab economy" and warned that these figures were based on projections of a "short but intense" conflict lasting only four weeks. The reality, as we now know, extended far beyond that timeframe.

The Energy Shock: The World's Most Critical Chokepoint

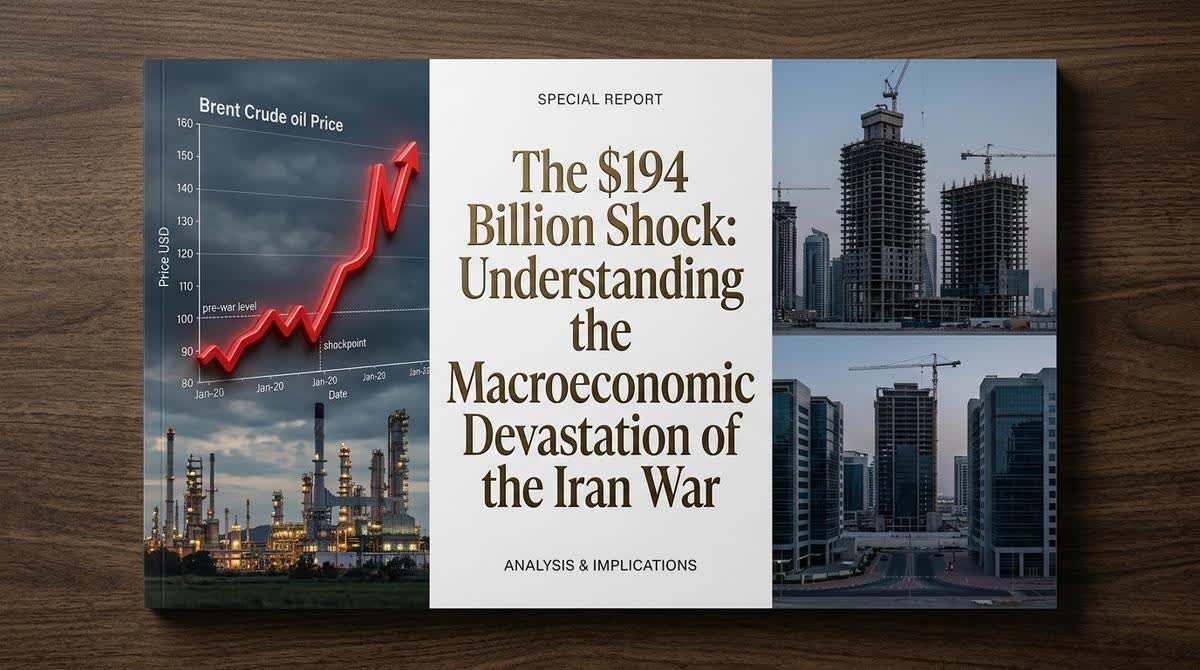

At the heart of the economic devastation was the effective blockade of the Strait of Hormuz, through which approximately 20 percent of the world's oil and gas exports pass. Iran's strategy of targeting this critical chokepoint, combined with direct attacks on oil and gas facilities across the Gulf, triggered the largest energy shock since the outbreak of the Ukraine war.

The numbers tell the story of the crisis:

Metric | Pre-War | Peak Crisis | Post-Agreement |

|---|---|---|---|

Brent Crude (per barrel) | ~$72 | $120 | ~$80 |

Jet Fuel (per barrel) | ~$105 | $210+ | ~$140 |

European Natural Gas (per MWh) | ~€31 | ~€62 | ~€41 |

The International Energy Agency (IEA) described the conflict as the "biggest energy security threat in history," estimating that global oil supply losses reached nearly 13 million barrels per day. The IEA also documented that 84 energy facilities across the region sustained damage, with 34 classified as seriously or completely damaged.

Some of these facilities, the IEA warned, may require at least two years to return to full production even if the strait reopened safely. Consultancy Rystad Energy estimated the repair costs for damaged energy infrastructure at between $34 billion and $58 billion.

The GCC: Disproportionately Affected

The Gulf Cooperation Council (GCC) countries, despite their vast oil wealth, were among the hardest hit by the conflict. The World Bank projected that GCC economic growth would fall from 3.9 percent in 2025 to near zero in 2026 before recovering as reconstruction efforts began. In April 2026, the World Bank further cut its growth forecast for the GCC from 4.4 percent to just 1.3 percent.

GCC Country | Key Impact | Financial Consequence |

|---|---|---|

Saudi Arabia | East-West pipeline capacity only covers ~25% of normal Hormuz volumes | Fiscal deficit of 5.3% of GDP in 2025; $156 billion in external borrowing |

UAE | Jebel Ali hub hit hard; tourism, aviation, property affected | More diversified economy, but significantly impacted |

Qatar | LNG exports interrupted | ~$4 billion loss from one-month interruption |

The war also exposed fundamental vulnerabilities in the GCC's economic model, which had been centered on political and economic stability to promote diversification. As one analyst noted, "The war has shattered the Gulf's image as a peaceful oasis, and restoring that image will be arduous". Sectors such as tourism, commercial travel, and artificial intelligence—on which these countries had based their economic transition plans—were "strongly undermined by the conflict".

The Tourism Collapse: A Case Study in Economic Vulnerability

The tourism sector, a cornerstone of economic diversification efforts across the region, experienced a catastrophic collapse. Financial analysis firm Moody's forecast that hotel occupancy in Dubai would plummet from 80 percent to 10 percent in the second quarter of 2026.

Dubai International Airport was struck by Iranian drones, and more than 30,000 flights to and from the Middle East were cancelled. Several airlines were still operating reduced schedules months later, with jet fuel prices nearly doubling year-on-year due to the blockage of the Strait of Hormuz.

The Global Inflationary Spiral

The energy shock quickly filtered through the broader global economy, increasing transportation expenses, electricity prices, industrial production costs, and agricultural input prices—particularly fertilizers. The World Bank forecast global inflation to rise to 4 percent in 2026 from 3.3 percent in 2025.

The International Monetary Fund (IMF) warned that under a severe scenario, global inflation could exceed 6 percent by 2027, with developing economies facing significantly larger impacts than advanced economies. In the United States, annual inflation in May 2026 rose to 4.2 percent, its highest level in more than three years.

The Costs Extend Beyond the Immediate Conflict

Even as peace agreements began to take shape, the economic damage continued to accumulate. The World Bank projected Brent crude oil prices to average $94 per barrel in 2026, around 36 percent higher than 2025 levels, even assuming the worst disruptions eased in July.

The conflict has also had a lasting impact on global commodity markets beyond oil. The price of fertilizer rose significantly, as much of the world's supply passes via the Gulf region. The price of helium, essential for manufacturing semiconductors, also increased, with over a third of global supply exported by Qatar. Disruption to smelter activity in the Gulf undermined aluminum production and exports.

The Strategic Implications for Business

For businesses operating in the Middle East, the macroeconomic devastation has several critical implications:

- Project Financing is Under Pressure:Â With GCC governments facing reduced revenues and increased reconstruction costs, capital for new infrastructure and technology projects is constrained.

- Operational Costs Have Spiked:Â Higher energy prices have increased the cost of powering data centers, running construction equipment, and transporting materials.

- Insurance and Risk Premiums Have Increased:Â The war has fundamentally altered the risk assessment for the region, with higher premiums for property, liability, and political risk insurance.

- Workforce Challenges:Â With millions of jobs lost and economic uncertainty, retaining skilled technical talent has become more difficult.

- Supply Chain Disruption:Â The attacks on ports and shipping routes have disrupted the flow of materials and equipment essential for infrastructure projects.

The Long View: Recovery and Reconstruction

Despite the devastation, there are signs of recovery. The US-Iran peace agreement has eased immediate fears in financial markets, and the reopening of the Strait of Hormuz is expected to restore some normalcy to energy markets.

However, economists warn that the conflict has already left a significant mark on the global economy through higher energy prices, rising inflation, weaker growth, and disruptions to commodity markets. The economic damage could outlive the military campaign itself.

The reconstruction effort will be massive, creating opportunities for companies with the capability to rebuild damaged infrastructure. The GCC countries are likely to accelerate their efforts to diversify their economies and reduce dependence on oil, creating long-term opportunities in technology, renewable energy, and digital infrastructure.